Throughout the course of history, governments that use fiat currency have overspent and eventually gotten themselves into dire situations with debt. Their response has never been to correct their errors and return to fiscal discipline, it has instead universally been to attempt to inflate their way out of trouble.

I bring this up because I've been trying to give honest consideration to some version of an actual bull case, and one version of that case involves completely ignoring the economic fundamentals and instead focusing on the Fed firing up the QE presses again anytime they feel they need to. We already know the Fed has been providing a ton of "back door" liquidity to the banking system, which likely staved off a broader collapse nearly a year ago when SVB (et al) failed.

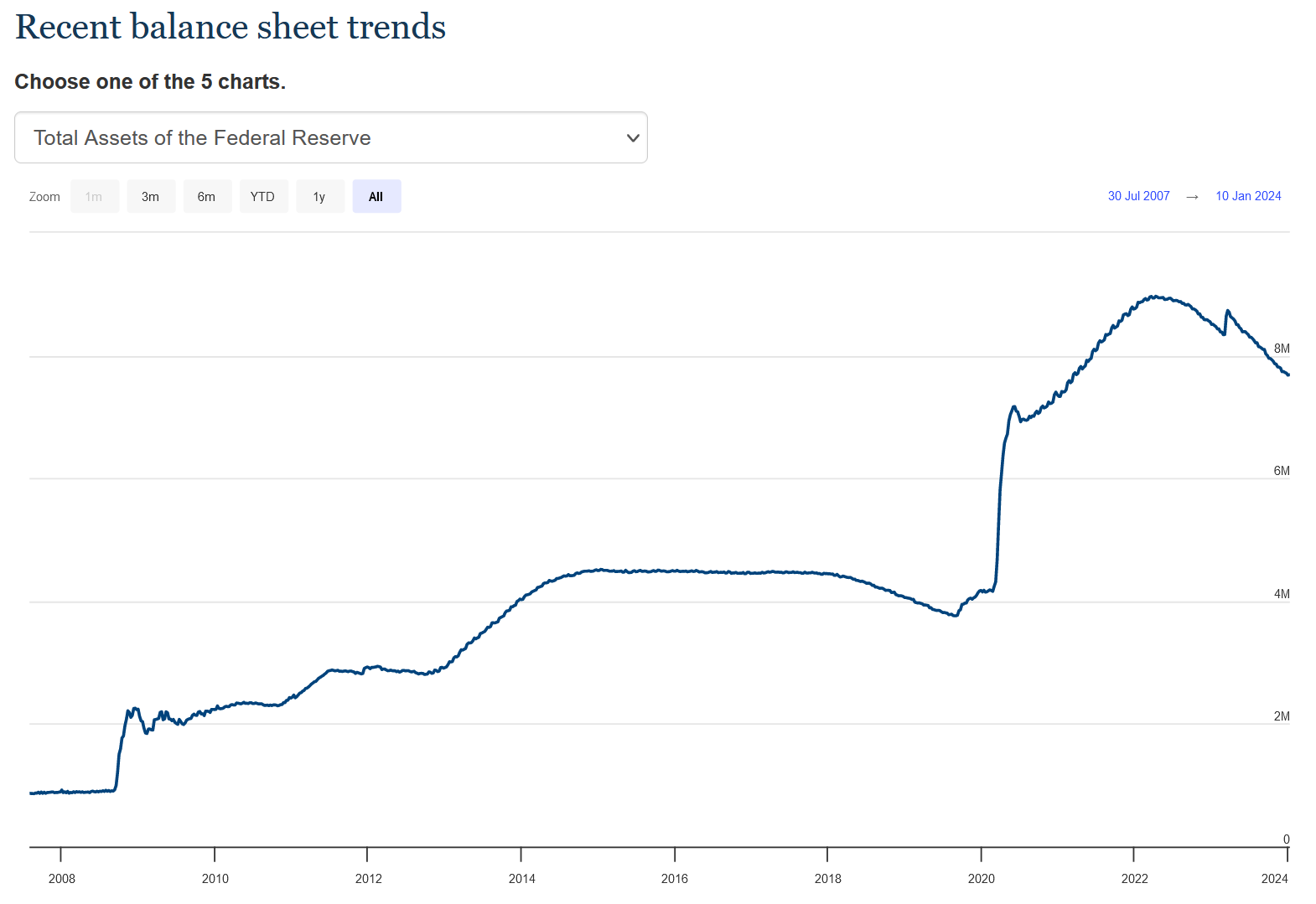

So maybe they can keep kicking this can even farther down the road than any of us want to imagine. We can see on the chart below that the Fed has managed to trim about $1.2 trillion off their public balance sheet, so far with minimal visible damage to the market, though, granted, this is a drop in the bucket vs. what's been added. But maybe this chart ends up looking like a staircase before it's all said and done: A trillion off here, then 4 trillion back on there, and so on.

If that, and/or similar things, were to happen, then they could inflate the market higher longer than seems reasonable. Though the long-term costs would be devastating to the American public, the short-term option of "not during my term in office!" has historically been too tempting to avoid.

I discussed this possibility on the forum more than a year ago, but I guess deep-down I keep hoping for a return to something approximating an actual free market, whether the Fed/government does so voluntarily or has their hand forced by circumstance. But maybe that hope is still premature and this game needs longer to play out.

I think that's the bull case.

Because the market has already priced in the "soft-landing" outcome and is now further banking on no recession, even though one might say those hopes are also premature, since recessions typically don't show up until 7-16 quarters after the first rate-hike -- and we're just barely at the lowest end of that timing range now.

Chart-wise, I drew up another longer-term chart illustrating one bull option that I'd only discussed verbally in prior updates:

And futures are indicating that SPX was indeed a b-wave high:

I'm about out of time for today. Trade safe.

No comments:

Post a Comment